Decreasing Life Cover

Decreasing Life Cover

Decreasing Life Cover

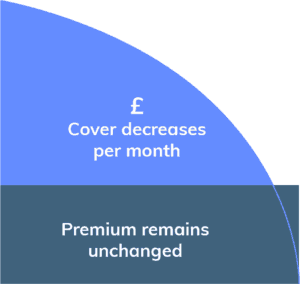

Decreasing Life CoverDecreasing cover life insurance is a type of cover that helps if you have a repayment mortgage or other sizeable reducing debt. The longer your cover is in place, the less is paid out. This is because your debts are also decreasing, and the insurance is there to help cover these payments. The monthly premiums for this type of policy may also be lower.

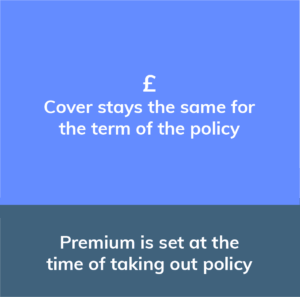

If you have an interest-only mortgage, you might be more interested in level-term life insurance. This is where payouts are fixed and the policy is in place for a pre-determined amount of time. The advantage of this kind of cover is that your family’s payout would be the same whether you died a year into your policy or a year before it expired.

The type of policy that you take out could be single – i.e. only covering you – or joint. A joint policy is usually cheaper than purchasing two single policies, but in most instances it only pays out once, if you make a claim you are no longer covered – the surviving partner would need to take out their own individual policy after that.

Two single policies can pay out upon the deaths of each policy holder and can take away the complexity in the unfortunate circumstance that the relationship comes to an end.

Level Term Cover

Level Term Cover

Level Term Cover

Level Term CoverLevel cover term insurance are policies which pay out lump sums if you die within your agreed term. If you wish to leave a sum of money to your kids rather than pay off debts, then consider an increasing or level term policy.