Life insurance

Life insurance eases your family's financial burden by covering mortgage payments in the event of your death.

Clever Mortgages is now part of Oak Mortgages Limited.

Don’t worry, you’ll still be looked after by the same friendly, experienced team you know and trust. We’re here to guide you every step of the way on your mortgage journey.

👉 Discover more about us at www.oakmortgages.co.uk or see what our happy clients are saying on Google Reviews.

EXCELLENTTrustindex verifies that the original source of the review is Google. Vicki and the team were amazing. They made the whole process so easy and straight forward. They were always very clear and proactive with communication. Highly recommended.Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience of Oak Mortgages has been unfailingly amazing. Abby is WONDERFUL at her job: super-kind, expert and patient and a huge credit to the company.Posted on GoogleTrustindex verifies that the original source of the review is Google. Highly professional and friendly.most of all given me the best advice and support along the process of my mortgage.Posted on GoogleTrustindex verifies that the original source of the review is Google. Claire was absolutely super to deal with from start to finish. As a first time buyer in both a slightly complex situation, and also under time constraints, she went above and beyond in finding a workable solution. As someone who both hates and is fairly useless at admin, the whole process couldn’t have been made any easier for me. 100% recommendation. Thanks ClairePosted on GoogleTrustindex verifies that the original source of the review is Google. Great mortgage company!Posted on GoogleTrustindex verifies that the original source of the review is Google. We can't recommend Oak Mortgages enough! In particular Abby, who from the start was always super positive, kind and supportive. Incredibly friendly and nothing was too much bother. We're classed as a complex case and didn't think it would be possible us to remortgage and release funds but Abby managed to find us a really good deal and we were successful with our remortgage. Special thanks to Abby for all the help, we couldn't have done it without her. Even when we were dealing with other members of staff at Oak Mortgages, they were all really kind and approachable. Thank you!Posted on GoogleTrustindex verifies that the original source of the review is Google. Really happy with the service abby has gone above and beyond to help me as soon as i have decided on my dream home I will be using the service 1000%Posted on GoogleTrustindex verifies that the original source of the review is Google. Very professional and supportive staff. A high quality of service and would recommend them to anyone looking to find a new mortgage.Posted on GoogleTrustindex verifies that the original source of the review is Google. Oak Mortgages were amazing throughout our house sale & purchase. Abbey in particular was great, answering any questions we had promptly and providing a friendly service.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more

Life insurance

Life insurance can help your family to cope in the event of your death. Your life insurance can be used to pay off some or all of your mortgage. This can take the financial burden from them, giving them one less thing to worry about.

Protect against the unexpected

Life can be unpredictable. That’s why it’s best to prepare yourself for any eventuality, especially when it can impact your loved ones. At Clever Mortgages we can help you find the right type of life insurance to suit you.

If you die without life insurance and have any existing debts, including your mortgage, these will automatically be passed to your next of kin. This can leave your family with financial difficulties, especially if they depend on you as the main income provider or form of childcare. Life insurance acts as a safety net, protecting the ones you love the most if something were to happen to you.

What is life insurance?

Life insurance is a type of insurance that will only pay out in the event of your death. It can’t be used as a savings or investment product and has no cash value unless a valid claim is made.

You can choose the amount of cover you need and how long you will need it for. In return, you and your family will have peace of mind that if something happens to you, they would still be able to keep their home and have financial security.

What about illness or injury?

Life insurance won’t pay out in the event of an illness, accident or disability. To cover for these types of circumstances you should have a look at our critical illness cover and income protection insurance.

Types of life insurance

There are two main types of life insurance; whole-of-life and term life insurance. The type of insurance that is most suitable for you will depend on your situation. If you’re unsure what type of insurance you need, we can work with you to help you get the right product.

Whole-of-life insurance

As the name suggests, a whole-of-life policy will guarantee to pay out whenever you die. This option is typically the most expensive type of life insurance because a claim is inevitable.

Term life insurance

Term life insurance will only pay out during the fixed period set within your policy. This is the most common form of life insurance, as many people only require a payout if they die whilst their mortgage hasn’t been paid off.

There are different types of term life insurance depending on your situation:

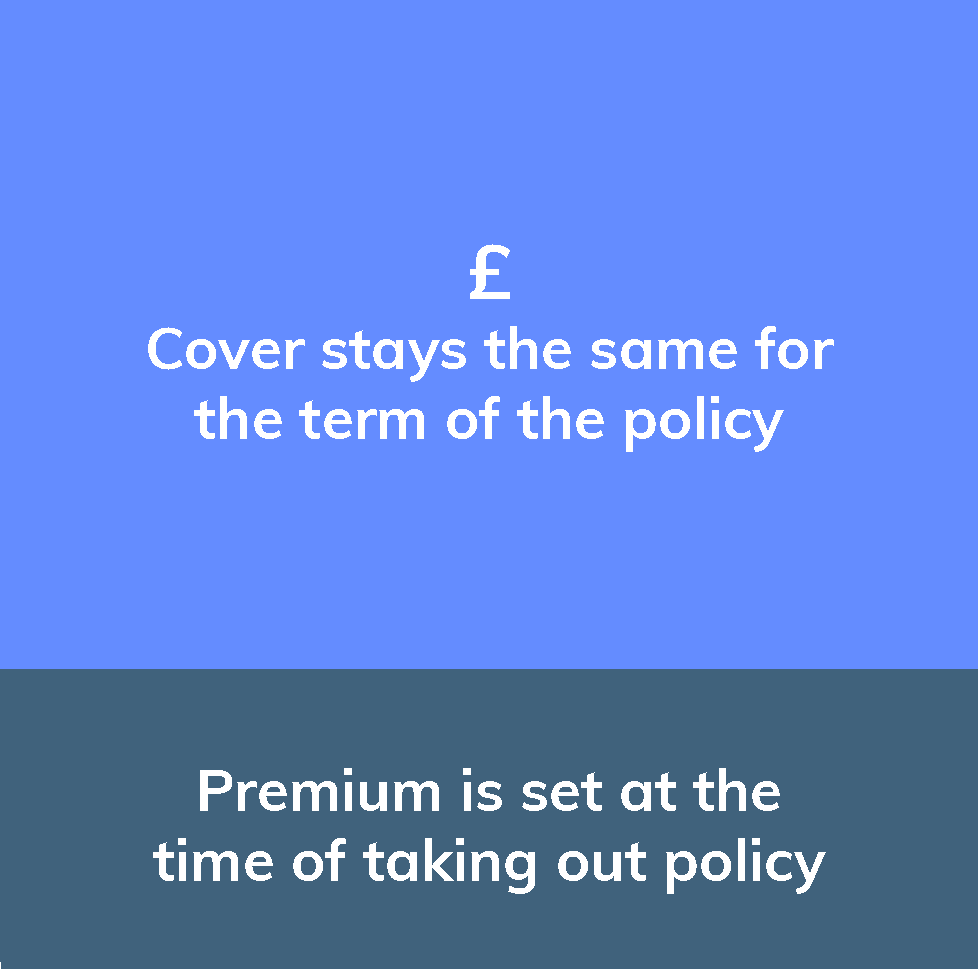

Level term policy

This policy will pay the same amount throughout the entire term unless you change it during that time. With this policy, you will know exactly what your family will be left with in the event of your death.

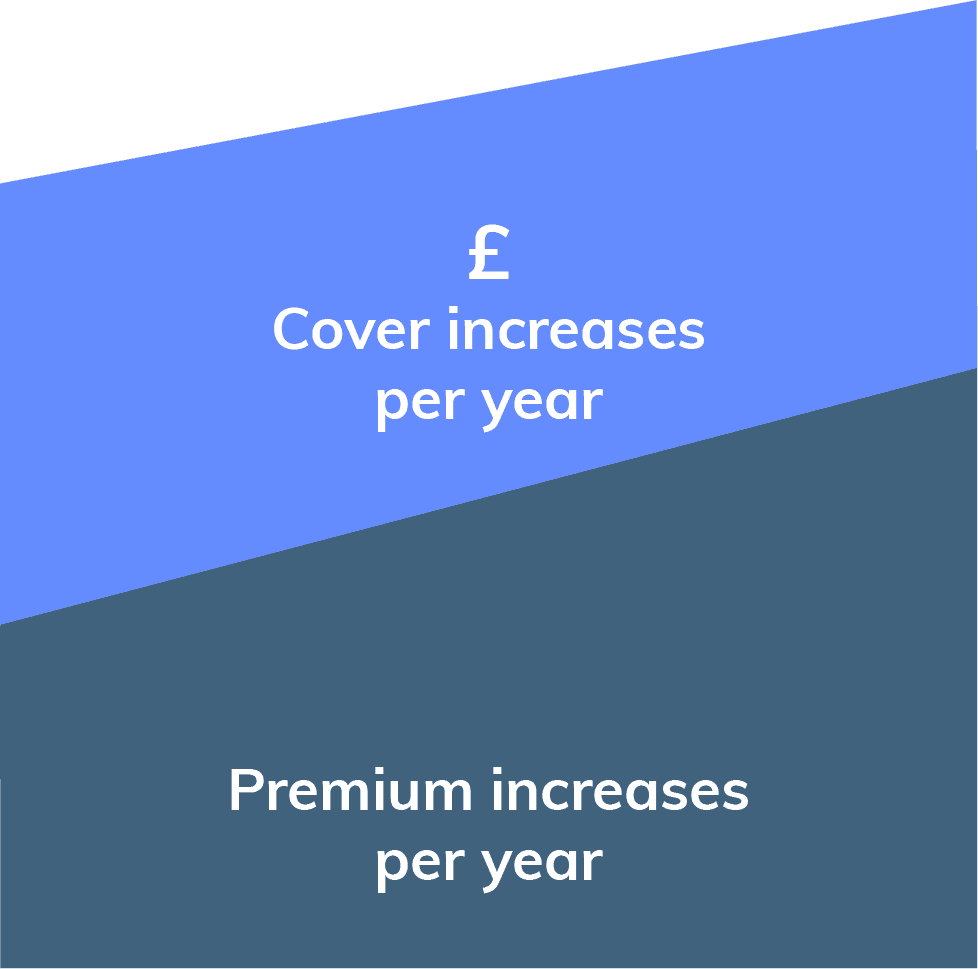

Increasing term policy

An increasing term policy factors in the rising cost of living. Any money paid out will be in line with the Retail Prices Index (RPI), ensuring that the money insured holds is real value throughout the term. However, as the amount insured rises over time, so will the premiums in line with this. Therefore, if you decide this policy is right for you, you should be prepared to pay more as time goes on.

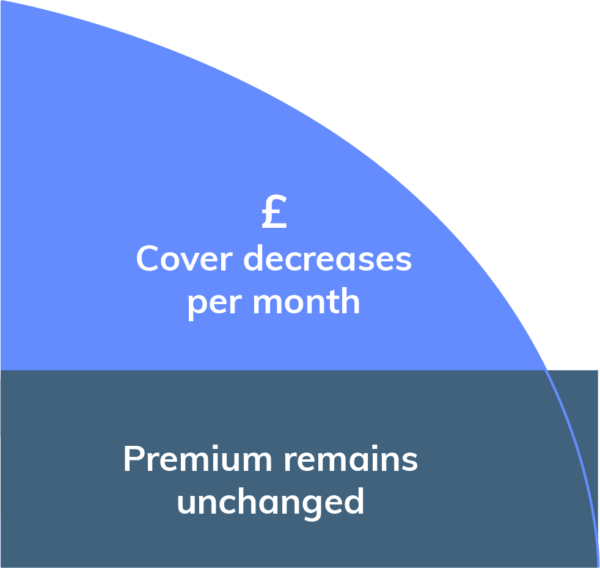

Decreasing term policy

Decreasing term insurance is designed to cover a debt that will gradually reduce over time, such as a mortgage. With this type of insurance, your monthly payments will stay the same, but the overall mortgage debt will decrease. The amount that the insurance company will pay out will also decrease to reflect the remaining debt on your mortgage.

How much does life insurance cost?

The cost of life insurance depends on a number of factors including the policy you take out as well as your age, lifestyle and medical history. So if you are young, active and healthy then, in general, you will pay less for life insurance than someone who is older or someone who has a life-long medical condition.

Clever Mortgages is now part of Oak Mortgages Limited.

Don’t worry, you’ll still be looked after by the same friendly, experienced team you know and trust. We’re here to guide you every step of the way on your mortgage journey.

👉 Discover more about us at www.oakmortgages.co.uk or see what our happy clients are saying on Google Reviews.

EXCELLENTTrustindex verifies that the original source of the review is Google. Vicki and the team were amazing. They made the whole process so easy and straight forward. They were always very clear and proactive with communication. Highly recommended.Posted on GoogleTrustindex verifies that the original source of the review is Google. My experience of Oak Mortgages has been unfailingly amazing. Abby is WONDERFUL at her job: super-kind, expert and patient and a huge credit to the company.Posted on GoogleTrustindex verifies that the original source of the review is Google. Highly professional and friendly.most of all given me the best advice and support along the process of my mortgage.Posted on GoogleTrustindex verifies that the original source of the review is Google. Claire was absolutely super to deal with from start to finish. As a first time buyer in both a slightly complex situation, and also under time constraints, she went above and beyond in finding a workable solution. As someone who both hates and is fairly useless at admin, the whole process couldn’t have been made any easier for me. 100% recommendation. Thanks ClairePosted on GoogleTrustindex verifies that the original source of the review is Google. Great mortgage company!Posted on GoogleTrustindex verifies that the original source of the review is Google. We can't recommend Oak Mortgages enough! In particular Abby, who from the start was always super positive, kind and supportive. Incredibly friendly and nothing was too much bother. We're classed as a complex case and didn't think it would be possible us to remortgage and release funds but Abby managed to find us a really good deal and we were successful with our remortgage. Special thanks to Abby for all the help, we couldn't have done it without her. Even when we were dealing with other members of staff at Oak Mortgages, they were all really kind and approachable. Thank you!Posted on GoogleTrustindex verifies that the original source of the review is Google. Really happy with the service abby has gone above and beyond to help me as soon as i have decided on my dream home I will be using the service 1000%Posted on GoogleTrustindex verifies that the original source of the review is Google. Very professional and supportive staff. A high quality of service and would recommend them to anyone looking to find a new mortgage.Posted on GoogleTrustindex verifies that the original source of the review is Google. Oak Mortgages were amazing throughout our house sale & purchase. Abbey in particular was great, answering any questions we had promptly and providing a friendly service.Verified by TrustindexTrustindex verified badge is the Universal Symbol of Trust. Only the greatest companies can get the verified badge who has a review score above 4.5, based on customer reviews over the past 12 months. Read more